Mean reversion is the market’s tendency to move back toward a more “normal” range after drifting too far in one direction. It is not a perfect law and it does not work the same way in every regime, but it becomes especially influential when markets move from smooth expansion into a more complex, late-cycle and consolidation environment. The year 2026 carries many signals of this shift. Instead of long, clean trends powered by abundant liquidity and one-directional narratives, markets are more likely to swing between extremes, overshoot, correct, and repeatedly return toward equilibrium.

This does not mean trends disappear. It means that the market’s dominant rhythm may shift toward oscillation, with rallies and sell-offs that fade more often than they extend.

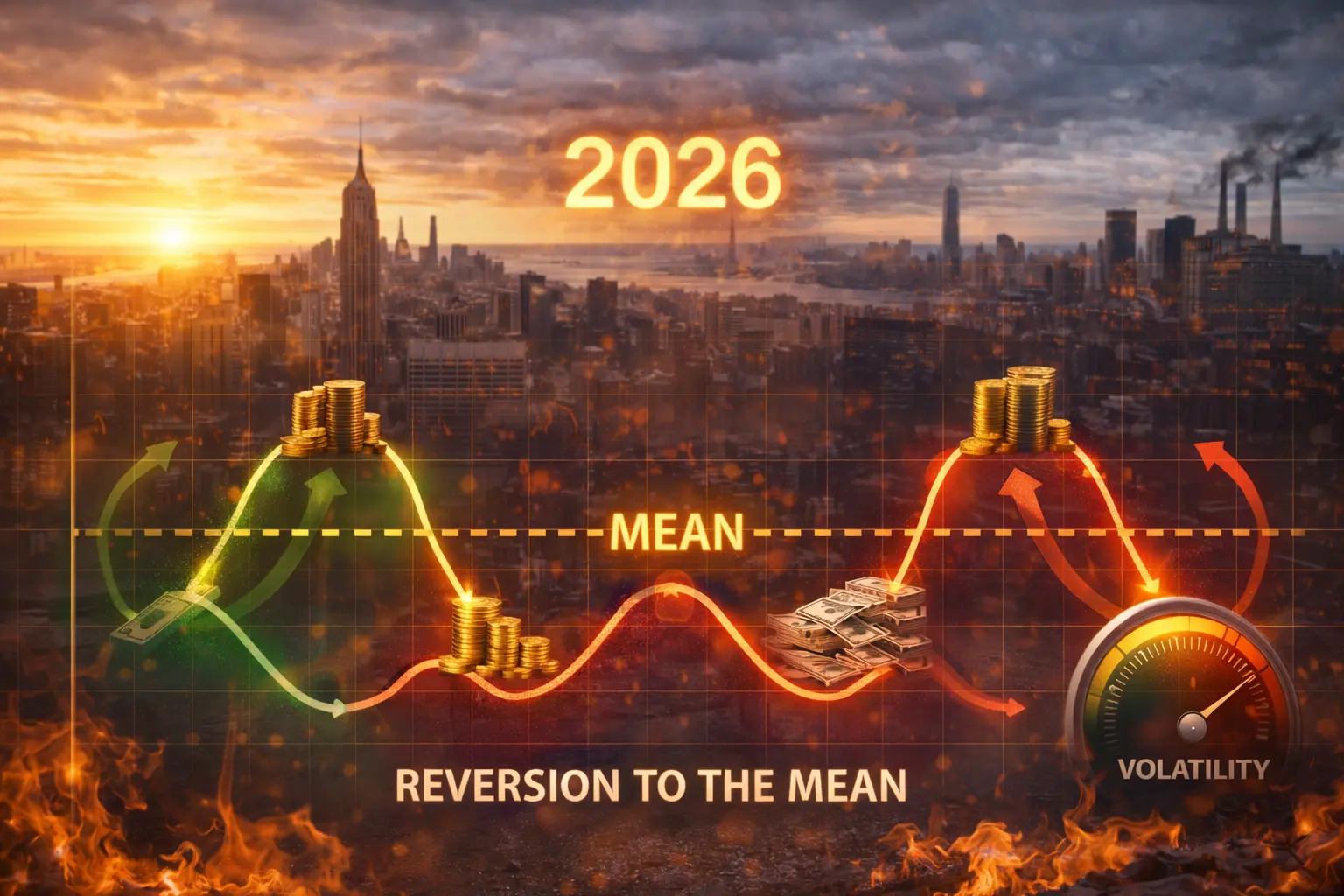

Mean Reversion as a Regime, Not a Tactic

Most investors think of mean reversion as a short-term trading idea. In reality, mean reversion can become a market regime, shaping how prices behave across weeks and months. In a mean-reversion regime, directional conviction weakens. Breakouts fail more frequently. Strong moves invite counter-moves as capital rotates quickly and risk limits tighten.

In 2026, several structural forces make a mean-reversion regime more likely. Liquidity is less forgiving, volatility clusters, and narratives rotate faster. As a result, markets often move too far too fast, then snap back, not because fundamentals changed overnight, but because positioning and risk tolerance changed.

Mean reversion becomes dominant when markets stop trending smoothly and start behaving like a system constantly searching for balance.

Why Easy-Money Trends Lose Their Power

Long, persistent trends flourish when liquidity is abundant and capital is cheap. In that environment, investors can hold risk longer, leverage can stay elevated, and dips are bought reflexively. When capital becomes more expensive and liquidity becomes conditional, trend persistence weakens.

In 2026, higher sensitivity to rates, tighter financial conditions, and faster sentiment shifts reduce the durability of trends. Moves still happen, but they are interrupted more often. The market becomes quicker to question itself and quicker to punish crowded positioning.

This naturally favors mean reversion because sustained one-way moves become harder to maintain.

Structural Volatility Creates Overshoots That Must Correct

A structural volatility regime increases the frequency of overshoots. Prices move beyond what fundamentals justify because liquidity thins, fear spikes, or enthusiasm becomes excessive. When overshoots become common, mean reversion becomes common as well, because markets repeatedly need to correct these extremes.

In 2026, the combination of constrained policy backstops, geopolitical uncertainty, and unstable narratives makes volatility more persistent. Volatility is the fuel that creates mispricings. Mean reversion is the mechanism that corrects them.

When markets overshoot often, mean reversion becomes the dominant rhythm.

Crowded Positioning and the Snap-Back Effect

Mean reversion strengthens when positioning becomes crowded. Crowding builds when investors cluster into similar trades, themes, or factor exposures. When a trade becomes too crowded, the market becomes vulnerable to sudden reversals because even small shocks trigger de-risking.

In 2026, the speed of information and capital movement increases the probability of crowding and the frequency of unwind events. These unwinds often look like mean reversion, where an extended move quickly retraces.

Crowding does not just create volatility. It creates snap-back behavior, a classic mean-reversion signature.

The Return of Range-Bound Markets

Mean reversion thrives in range-bound markets. When indices and major assets trade sideways over time, they still produce strong moves within that range. These moves often reverse when they hit the boundaries of valuation, liquidity, or sentiment.

In 2026, consolidation dynamics and regime uncertainty increase the probability of range-bound behavior. Markets may spend longer “digesting” rather than breaking into new sustained trends. During digestion, swings become tradable and trends become fragile.

Range-bound conditions encourage investors to sell strength and buy weakness, the behavioral foundation of mean reversion.

Why Correlation Shifts Reinforce Mean Reversion

When correlations are unstable, diversification becomes less reliable, and capital shifts more frequently between assets. These rotations can cause short bursts of momentum, followed by reversals as money moves to the next relative opportunity.

In 2026, correlations may become more conditional due to shifting inflation and policy narratives. As the dominant market fear changes, leadership changes quickly. This creates rotational behavior rather than stable trend leadership.

Rotation reinforces mean reversion because winners and losers swap more frequently than in clean-trend regimes.

Mean Reversion and Valuation Sensitivity

A higher cost of capital increases valuation sensitivity. When valuations stretch, markets become quicker to correct because future cash flows are discounted more aggressively. When valuations compress too far, value-hunting and short covering can drive sharp rebounds.

In 2026, valuation sensitivity is stronger than in the ultra-low rate era. This sensitivity creates natural boundaries that encourage prices to revert. It also increases the speed of correction when prices move beyond those boundaries.

Mean reversion is often the market’s way of enforcing valuation discipline when liquidity is not willing to support extremes for long.

The Role of Macro Uncertainty in Shortening Trend Duration

Macro uncertainty shortens trend duration because investors lack conviction to hold directional bets for long. When inflation, rates, geopolitics, and policy are all uncertain, market participants reduce time horizons.

In 2026, shorter time horizons mean profits are taken faster, losses are cut faster, and moves are faded more often. This reduces trend persistence and increases the frequency of reversals.

Mean reversion dominates when conviction is low and horizon is short.

How Mean Reversion Appears Across Asset Classes

Mean reversion is not limited to equities. It appears across commodities, currencies, rates, and digital assets when conditions favor oscillation. In 2026, cross-asset linkages and global capital flows can cause synchronized overshoots and synchronized corrections.

When investors shift into safety, multiple assets reprice together. When risk appetite returns, they rebound. These repeated shifts create mean-reverting behavior across markets.

A mean-reversion regime can therefore be broad, affecting many asset classes simultaneously.

How Investors Should Adapt to a Mean-Reversion Dominant Year

When mean reversion dominates, investors should adjust expectations and behavior. In a trending market, holding winners works. In a mean-reverting market, chasing breakouts often fails and overcommitting at extremes becomes costly.

This does not require constant trading. It requires better timing discipline, patience, and an understanding of extremes. Investors benefit from recognizing when markets are stretched, when sentiment is one-sided, and when liquidity conditions suggest reversal risk.

In 2026, the investor advantage may come from avoiding emotional chasing and from treating extremes as information.

Why Mean Reversion Is a Natural Late-Cycle Behavior

Late-cycle markets often exhibit mean reversion because leadership narrows, volatility increases, and confidence becomes unstable. 2026 contains many of these features. Even if markets produce rallies, those rallies may be interrupted by pullbacks that correct excess.

Mean reversion is therefore not a prediction of weakness. It is a description of rhythm. The market can still generate returns, but it does so through swings rather than through smooth compounding.

Annual Letter 2026 by Rajeev Prakash Agarwal

Markets are entering a phase where easy assumptions no longer work. Liquidity is selective, volatility is structural, and capital is rewarded only when it is positioned with clarity and discipline. In such an environment, reacting to headlines is not enough. What matters is having a forward-looking framework that helps you anticipate change rather than chase it.

The Annual Letter 2026 by Rajeev Prakash Agarwal offers a comprehensive investment outlook designed for this new market regime. It blends long-term macro analysis, market psychology, and planetary cycles that have historically aligned with major shifts in global capital flows. The focus is on understanding cycles, identifying high-probability phases, and protecting capital during periods of uncertainty.

The Opportunity Inside Mean Reversion

Mean reversion creates opportunity because it produces repeated mispricings. Fear and greed push prices away from reasonable levels. Mean reversion pulls them back. Investors who remain disciplined can use this rhythm to improve entry quality, reduce drawdowns, and avoid being trapped in crowded trades at the wrong time.

In 2026, where calm markets may be rare and narratives may change quickly, mean reversion offers a framework for understanding why markets behave inconsistently. It explains why moves often reverse after feeling convincing.

Mean reversion will dominate markets in 2026 because the environment favors oscillation over persistence. Liquidity is less forgiving, volatility is structural, and conviction is shorter-lived. Investors who understand this regime will stop chasing certainty and start reading extremes as signals. In a year defined by reversals, discipline becomes the strategy, and patience becomes the edge.

Mean Reversion Thrives When Confidence Is Fragmented

Another reason mean reversion is likely to dominate markets in 2026 is fragmented confidence. In earlier cycles, investors shared broadly similar expectations about growth, inflation, and policy. That collective belief allowed trends to persist. In 2026, confidence is fragmented. Different participants hold sharply different views, and those views shift rapidly as new information emerges.

This fragmentation creates constant push and pull in prices. When one camp gains conviction, prices move quickly. When opposing views regain influence, prices retreat. Neither side maintains dominance long enough for sustained trends to develop.

Fragmented confidence naturally produces mean-reverting behavior.

Mean Reversion and the Breakdown of Buy-and-Hold Assumptions

Buy-and-hold strategies work best in long, trending markets with stable leadership and supportive liquidity. In a mean-reversion regime, buy-and-hold becomes more uneven. Returns may still be positive over time, but the path is rougher, with frequent drawdowns and recoveries.

In 2026, investors relying purely on passive exposure may find the experience psychologically challenging. Price swings can be large relative to net progress. This does not invalidate long-term investing, but it does highlight the importance of risk management and entry discipline.

Mean reversion exposes the cost of ignoring timing entirely.

The Role of Risk Parity and Systematic Strategies

Systematic and risk-parity strategies respond mechanically to changes in volatility and correlation. When volatility rises, exposure is reduced. When volatility falls, exposure increases. In a structural volatility environment, this creates repeated cycles of de-risking and re-risking.

In 2026, these mechanical flows can amplify mean reversion. Rising volatility triggers selling, which pushes prices below equilibrium. When volatility subsides, buying resumes, pulling prices back. This pattern reinforces oscillation rather than trend continuation.

Systematic strategies do not cause mean reversion alone, but they accelerate it.

Mean Reversion as a Consequence of Policy Ambiguity

Clear policy direction supports trends. Ambiguous policy supports reversals. In 2026, policy ambiguity is likely to remain elevated due to competing objectives around inflation, growth, financial stability, and political pressure.

Markets react to policy signals, then reassess as interpretations change. Each reassessment can reverse prior moves. Without a strong policy anchor, trends struggle to persist.

Policy ambiguity strengthens the case for mean reversion dominance.

Why Extremes Become Short-Lived

In a mean-reversion regime, extremes do not last long. Overbought conditions attract profit-taking. Oversold conditions attract bargain-hunting and short covering. The speed of modern markets accelerates this process.

In 2026, information travels quickly, and positioning adjusts rapidly. This reduces the lifespan of extremes. Investors who expect extended euphoria or prolonged panic may be disappointed.

Short-lived extremes are a defining feature of mean reversion.

The Interaction Between Volatility and Mean Reversion

Volatility and mean reversion reinforce each other. Volatility creates price dislocations. Mean reversion corrects them. The correction process itself can be volatile, creating further dislocations.

In 2026, this interaction produces a choppy market environment where direction is hard to sustain. Large candles are followed by retracements. Convincing moves fail more often than they succeed.

Understanding this interaction helps investors avoid misinterpreting volatility as the start of a new trend.

Mean Reversion Across Time Frames

Mean reversion in 2026 may operate across multiple time frames. Short-term moves may revert within days. Medium-term moves may revert over weeks. Even longer-term themes may experience extended periods of sideways consolidation rather than sustained advance.

This multi-time-frame mean reversion complicates strategy selection. Investors must align their approach with their time horizon and risk tolerance.

Misalignment between horizon and regime increases frustration.

Why Forecast Precision Loses Value

Mean reversion reduces the value of precise forecasts. When markets oscillate, being correct about direction is less important than managing exposure around extremes. Forecasts that rely on smooth continuation underperform in choppy regimes.

In 2026, investors benefit more from adaptability than from conviction. They focus on probability ranges rather than single outcomes.

Mean reversion rewards flexibility over certainty.