Multi Asset Investment Strategy: Building Resilient Portfolios Across Cycles, Rates, and Regimes

Multi asset investing is the disciplined practice of allocating capital across more than one asset class so a portfolio can survive different market environments, not just thrive in one good year. A strong multi asset investment strategy recognizes a simple truth: equities do not always lead, bonds do not always hedge, cash is not always safe in real terms, and alternatives are not always diversifiers. The goal is not to predict the future perfectly. The goal is to build a portfolio that can adapt, absorb shocks, and still compound wealth over time.

Investors often begin with a single market story. They might believe technology stocks will always outperform, or that government bonds always protect, or that gold always rises when uncertainty increases. In reality, markets rotate leadership. Inflation regimes flip. Growth scares appear and disappear. Currency cycles turn. Liquidity conditions tighten and loosen. A multi asset approach is designed for this rotation. It builds a portfolio that does not depend on one asset, one sector, one country, or one narrative.

This article explains how multi asset portfolios work, why diversification sometimes fails, how to design allocations that match your objectives, and how to manage risk through cycles. It also covers practical portfolio frameworks, rebalancing discipline, and common mistakes that quietly destroy long term results.

What a Multi Asset Investment Strategy

A multi asset strategy is more than holding several funds. It is a complete investment framework that balances return engines, defensive ballast, and optionality. It combines assets that respond differently to growth, inflation, interest rates, credit conditions, and risk appetite. In a well structured portfolio, some exposures are meant to grow in favorable periods

Most investors already understand the headline idea of diversification. What they often miss is that diversification is not just about owning many things. It is about owning the right mix of things, in the right proportions, with a clear reason for each holding. If you own ten equity funds that all tilt toward the same growth style and the same mega cap names, you are not diversified. You are concentrated with extra steps.

A true multi asset strategy answers four questions clearly. What outcomes are you targeting. What risks can you tolerate. What time horizon do you have. What constraints must you respect, including liquidity needs, taxes, and drawdown tolerance.

Why Multi Asset Investing Matters More

In earlier decades, a simple portfolio could sometimes work for long stretches. A classic mix of equities and high quality bonds delivered strong results because disinflation supported bond prices and equity valuations. However, macro conditions evolve. Inflation can reappear. Central banks can keep rates higher for longer. Fiscal dynamics can change the behavior of government bonds. Globalizations can reverse in pockets. Technology and geopolitics can reshape supply chains. All of this means that a single static allocation may not behave the way it did in the past.

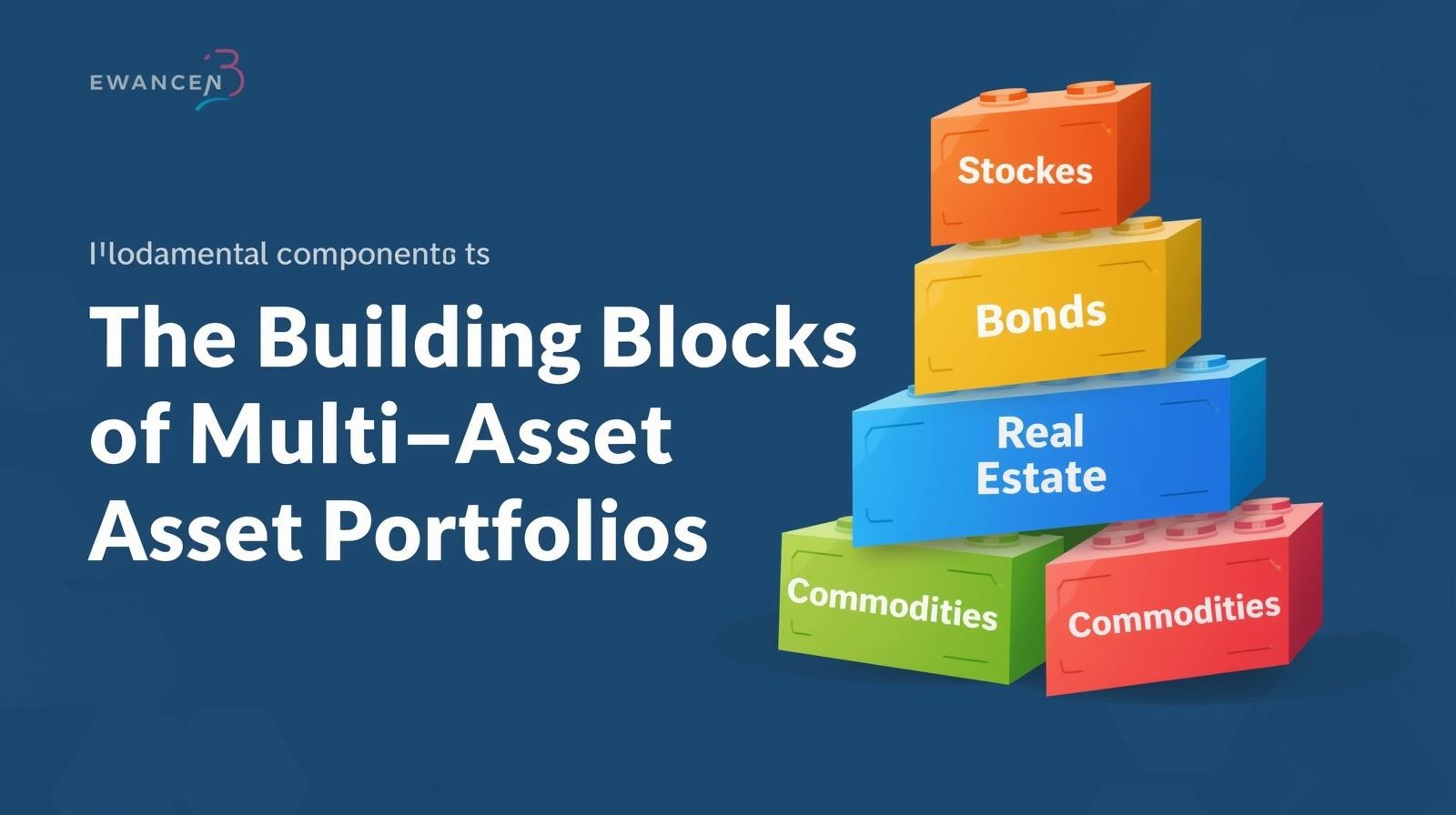

The Building Blocks of Multi Asset Portfolios

Equities represent ownership of productive businesses and are often the primary long term growth engine. They tend to perform best when growth expectations rise and financial conditions are supportive. Within equities, diversification matters across regions, sectors, and styles, such as value and growth.

The Two Big Drivers: Regime and Correlation

Most portfolio outcomes come from how assets behave together, not just how each asset performs individually. Investors often assume correlations are stable. They are not. Correlations can compress toward one during crises, meaning many risky assets fall together. Correlations can also shift across regimes, especially between equities and bonds.

Strategic Asset Allocation: The Foundation

Strategic asset allocation is the long term target mix of asset classes. An aggressive investor might allocate more to equities and growth oriented assets. A conservative investor might hold a larger share of bonds, cash, and quality income assets. A retiree might priorities income stability and drawdown control.

Tactical Asset Allocation: The Overlay

Tactical allocation is an active tilt away from the strategic mix based on valuations, macro signals, momentum, or risk conditions. Tactical decisions can improve results if executed with discipline. They can also destroy results if they become emotional market timing.

Risk Parity and Balanced Risk Approaches

Risk parity and balanced risk approaches aim to distribute risk more evenly across asset classes. This can reduce reliance on equities for returns and reduce drawdowns. However, risk parity often uses leverage to increase bond exposure, which can introduce its own risks,.

The Role of Inflation Protection

Inflation is one of the most underestimated long term threats. Even moderate inflation compounds into a meaningful loss of purchasing power. Multi asset portfolios often include explicit inflation hedges because bonds and cash may not protect real returns when inflation is elevated.

Liquidity and Rebalancing: The Hidden Edge

Rebalancing is one of the most powerful and underappreciated features of multi asset investing. It forces you to trim what has become expensive and add to what has become cheap, without relying on predictions.

Rebalancing works because markets overshoot in both directions. Over time, rebalancing can add a small return premium while controlling risk. The key is to rebalance with discipline rather than emotion.

There are different approaches. Time based rebalancing happens on a schedule, such as quarterly or annually. Threshold based rebalancing happens when an asset drifts beyond a set range from its target. Many investors use a hybrid approach.

Liquidity is critical for rebalancing. If your portfolio is filled with illiquid assets, you may not be able to rebalance when it matters most. A good multi asset strategy maintains enough liquid instruments so you can act during stress rather than freeze.

Income Generation Within a Multi Asset Strategy

Many investors want income. However, chasing yield can quietly increase risk. High yields often reflect higher credit risk, higher duration risk, or structural vulnerabilities.

A multi asset income strategy typically blends several income sources. Dividend equities can provide growing income over time but can still be volatile. Investment grade bonds provide steadier coupons but can lose value when yields rise. Real estate investment trusts can provide income but are sensitive to rates and economic activity. Preferred securities and high yield bonds can increase income but require careful sizing.

The best income approach is one that balances yield and resilience. It should also be flexible, because income needs can change across life stages.

Drawdown Control and Risk Budgeting

Most investors say they want higher returns, but what they truly struggle with is drawdowns. A large drawdown can lead to panic selling, which locks in losses and interrupts compounding.

A multi asset strategy should be designed with a clear drawdown tolerance. If a portfolio’s volatility is too high for your behaviour, the portfolio is not suitable, even if expected returns look attractive.

Risk budgeting is a useful concept. You allocate risk intentionally, not accidentally. You decide how much risk to allocate to equities, how much to rates, how much to credit, how much to inflation hedges, and how much to alternatives. You also decide how much tail risk you are willing to accept.

Some investors also use explicit risk controls such as volatility targeting or trend following overlays. These can reduce drawdowns but can also reduce returns during fast rebounds. If you use them, you must accept the trade off.

Common Multi Asset Portfolio Frameworks

There are several widely used frameworks for multi asset portfolios. The best choice depends on your objectives.

A growth focused balanced portfolio typically uses global equities as the primary return driver, supported by high quality bonds and some real assets. This suits long horizon investors who can tolerate volatility but want some ballast.

A defensive balanced portfolio increases bonds, cash, and quality income assets, and reduces equity exposure. It suits investors who prioritise capital preservation and stability.

An inflation aware portfolio includes a deliberate sleeve of commodities, inflation linked bonds, and real assets. It suits investors concerned about purchasing power and regime shifts.

An all weather style portfolio tries to hold assets that perform across multiple regimes, with careful sizing to avoid over concentration. It typically includes equities, bonds of varying durations, inflation hedges, and diversifiers such as managed futures.

A dynamic risk managed portfolio uses signals to adjust exposures as conditions change. This suits investors comfortable with a rules based approach and who can evaluate it over full cycles.

The key is to choose one framework and implement it with discipline rather than mixing several philosophies in a confusing way.

Selecting Instruments: Funds, ETFs, and Direct Holdings

Implementation matters as much as allocation. Costs, liquidity, taxes, and tracking error all influence results.

For many investors, low cost broad market funds are the simplest foundation. They provide exposure without requiring constant decisions. Active funds can add value in less efficient markets, but manager selection is hard and fees compound negatively.

If you use ETFs, check liquidity, spreads, and underlying holdings. For bond exposure, understand duration, credit quality, and sensitivity to rate changes. For commodity exposure, understand how the product gains exposure, because futures based products can behave differently than spot prices due to roll yield.

Direct holdings can work well if you have expertise and time, but concentration risk rises quickly. A multi asset strategy is often best implemented with diversified core holdings and limited satellites.

Behavioural Discipline: The Real Strategy

The biggest threat to a multi asset portfolio is not a bad year in markets. It is the investor abandoning the plan at the wrong time. Multi asset investing only works if you stay with the process through cycles.

That means having clear expectations. It means accepting that some holdings will look disappointing for long periods. Inflation hedges may lag in calm times. Bonds may look unexciting during equity booms. Cash may feel like a mistake until it becomes an advantage.

A good strategy prepares you emotionally as well as financially. It gives you a plan for what to do when markets fall. It tells you when to rebalance, when to hold steady, and what you will not do.

How to Evaluate a Multi Asset Strategy

Evaluation should focus on more than average returns. You should measure volatility, maximum drawdown, and performance across different regimes. You should also assess whether the strategy met your specific objectives, such as capital preservation, income stability, or inflation protection.

Avoid judging a strategy based on a short window. Multi asset portfolios are designed for full cycles. A portfolio that protects you during deep drawdowns may look less impressive in euphoric bull markets. That is not failure. That is design.

Also pay attention to real returns, not just nominal returns. A strategy that grows capital but loses purchasing power does not meet long term goals.

Mistakes That Undermine Multi Asset Portfolios

One common mistake is over diversification into similar risk exposures. If your portfolio holds many funds but all are equity heavy, you are not diversified.

Another mistake is ignoring duration risk. Investors often buy long bonds for stability without recognising that long duration can be volatile when yields rise.

A third mistake is chasing performance. Buying last year’s winner and selling last year’s loser is the opposite of rebalancing. It increases the chance of buying high and selling low.

A fourth mistake is relying on a single hedge. For example, assuming bonds will always protect equities can fail during inflation shocks. A resilient strategy includes multiple diversifiers.

Finally, many investors underestimate fees. Small fee differences compound over decades. Multi asset strategies can become expensive if layered with high fee funds and unnecessary complexity.

A Practical Way to Design Your Own Multi Asset Strategy

Start by defining your target outcome. Are you trying to maximize growth, generate income, preserve capital, or balance all three. Then define your time horizon and drawdown tolerance.

Next, choose a strategic allocation that you can stick with. Include a global equity core for long term growth, a quality bond or stability core for ballast, and an inflation aware sleeve if purchasing power is a meaningful concern. Add alternatives only if you understand their role and can access them efficiently.

Then define rebalancing rules and stick to them. Decide how often you will review the portfolio. Decide what conditions would cause changes and what will not.

Finally, write down your strategy in plain language. A strategy you can explain clearly is easier to follow. A strategy you cannot explain usually contains hidden risks.

Multi Asset Investing and Long Term Wealth

Multi asset investing is not about avoiding risk. It is about taking the right risks in a way that lets you stay invested. The investor who compounds steadily often beats the investor who seeks the highest returns but cannot tolerate the volatility.

A thoughtful multi asset investment strategy gives you a framework for uncertain futures. It accepts that cycles will change and that leadership will rotate. It builds resilience through diversification, risk budgeting, inflation awareness, and rebalancing discipline.

Meet Our Team

Get to know our dedicated team of experts. With a diverse range of skills and years of experience, we’re committed to providing you with the best market analysis and investment guidance.

Mr. Rajeev Prakash Agarwal

Founder

Expert in financial & personal astrology for 20 years+. Rajeev is a well-known astrologer based in central India who has a deep understanding of both personal and mundane astrology.

Mr. Shashi Prakash Agarwal

Technical Head

Shashi is a technology leader with a strong background in global business.He holds a B. Tech in Computer Science & MBA in Finance from Narsee Monjee Institute of Management Studies, one of the top B-Schools in India.

Whether you’re a seasoned investor or just starting out, our financial astrology tools can be tailored to your specific investment goals. Gain valuable insights to achieve your financial aspirations.

Address

1301, 13th Floor, Skye Corporate Park, Near Satya Sai Square, AB Road, Indore 452010

+91 9669919000

© All Rights Reserved by RajeevPrakash.com (Managed by AstroQ AI Private Limited) – 2025