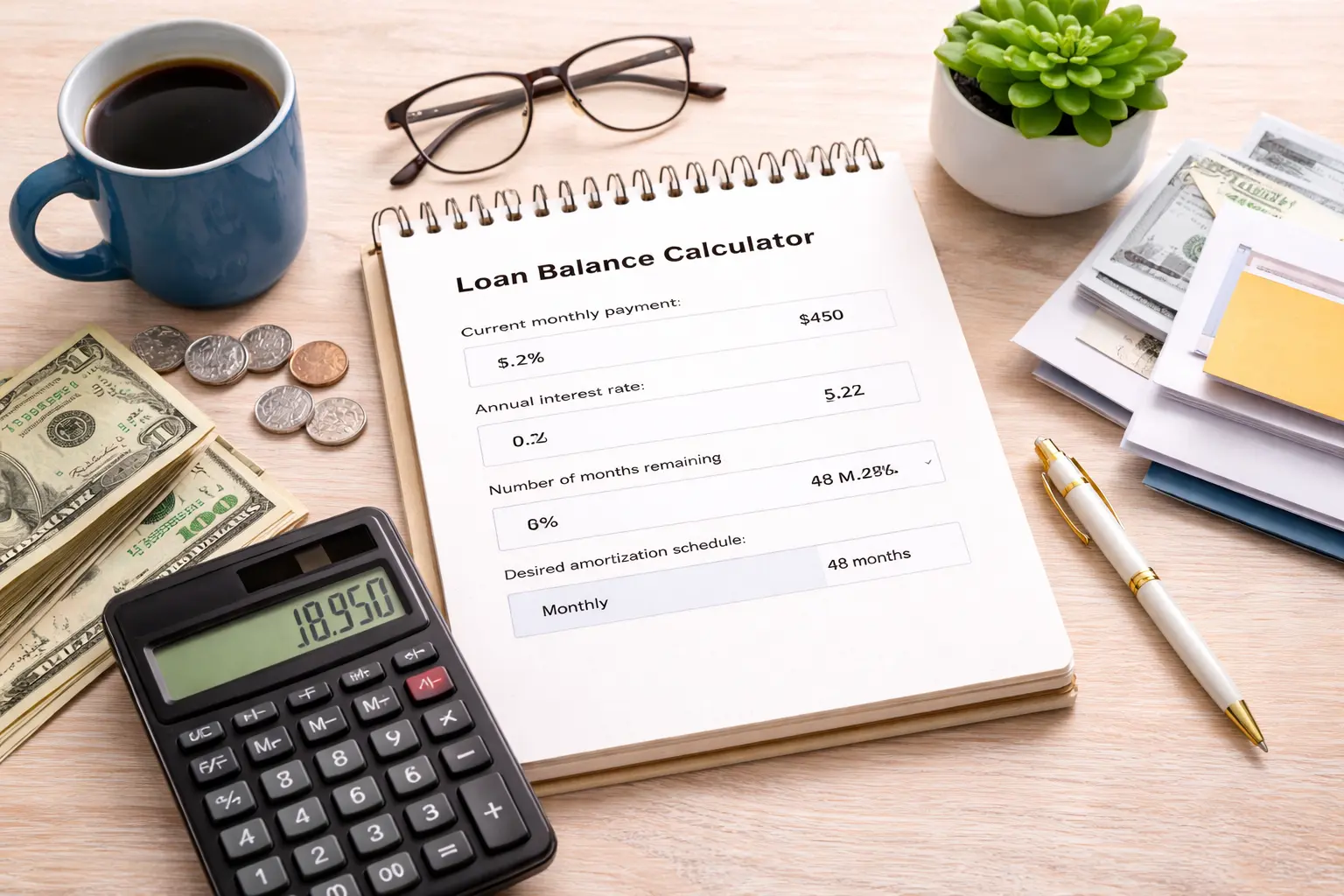

What is the balance on my loan?

Understanding the balance on your loan is a key step in managing your personal finances effectively. Many people focus only on the monthly payment and forget to track how much of the loan is still outstanding. This calculator allows you to estimate your current loan balance using information you already have, such as your payment amount, interest rate, and remaining term. It removes the guesswork involved in interpreting lender statements or older documents. By seeing an estimated balance, you gain a clearer picture of your financial position today. This is especially useful if your loan started years ago and you no longer have the original paperwork. Knowing your balance can also help you feel more confident when discussing options with lenders. Over time, regularly checking your estimated balance encourages better financial awareness and discipline.

What is the balance on my loan?

If you know your current payment, the interest rate and the term remaining, you can calculate your outstanding loan balance. Use this calculator to estimate the current loan balance and view an amortization schedule based on your selected frequency.

How this loan balance calculator works

Loan balances change every month as interest is added and payments are applied. The calculator uses standard amortization principles to recreate this process in reverse. It assumes a fixed interest rate and consistent payment schedule, which is common for many personal loans, auto loans, and mortgages. By applying your annual interest rate over the remaining number of months, the calculator estimates how much principal remains unpaid. This approach mirrors how lenders calculate balances internally. While the result may not match your statement to the last cent, it is close enough for planning and analysis. The calculation highlights how interest continues to affect your loan even when you are nearing the end of the term. It also shows why loans with higher interest rates decline more slowly. This understanding helps you see the true cost of borrowing over time.

Making sense of your monthly payment

Your monthly payment is more than just a fixed expense on your budget. Each payment includes an interest portion that compensates the lender and a principal portion that reduces your debt. Early in the loan term, a larger share of the payment goes toward interest. As the balance declines, the interest portion becomes smaller, and more of your payment reduces principal. This calculator uses your payment amount as a foundation for estimating the remaining balance. If your payment is only slightly higher than the interest charged, the balance decreases very slowly. Understanding this relationship can motivate you to increase payments when possible. Even small extra payments can shorten the loan term and reduce total interest. This insight can change how you view your monthly obligations.

Why the interest rate plays a major role

The annual interest rate has a powerful influence on how quickly your loan balance declines. A higher interest rate means more of each payment goes toward interest rather than principal. This calculator clearly demonstrates how interest affects your remaining balance over time. When comparing loans or considering refinancing, even a small reduction in interest rate can lead to meaningful savings. By adjusting the interest rate input, you can see how different scenarios impact your balance. This makes the tool useful not only for estimation but also for comparison. It helps you evaluate whether refinancing could be beneficial. Understanding interest also reduces the risk of taking on loans that appear affordable but are costly in the long run.

The importance of remaining loan term

The number of months remaining on your loan determines how much time you have to repay the balance. A longer remaining term spreads payments out, but it also allows more interest to accumulate. A shorter term accelerates repayment and reduces interest costs. This calculator uses the remaining months to determine how aggressively the balance is being paid down. If you are unsure about your payoff timeline, this tool provides clarity. It can also help you decide whether to shorten your loan term by making higher payments. Seeing how the balance changes with different timeframes encourages proactive planning. This awareness supports smarter decisions about debt management.

Using loan balance estimates for planning

An estimated loan balance is valuable for many financial decisions. It helps you assess whether you can afford to pay off a loan early or redirect funds to other goals. You can use the estimate to update your personal net worth calculations. It is also useful when planning large expenses or investments, as it clarifies your existing obligations. Lenders often ask for current balances during refinancing or consolidation discussions. Having a reliable estimate makes these conversations easier. This calculator acts as a planning tool rather than a replacement for official statements. Used regularly, it becomes part of a responsible financial routine. It supports long-term financial stability by keeping your debt in perspective.