A covered call is a simple, rules-based way to generate extra income from stocks you already own. You hold the shares and sell a call option against them, collecting premium in exchange for capping some upside. This guide explains setup, payoffs, Greeks, risks, and a checklist you can apply today.

What Is a Covered Call?

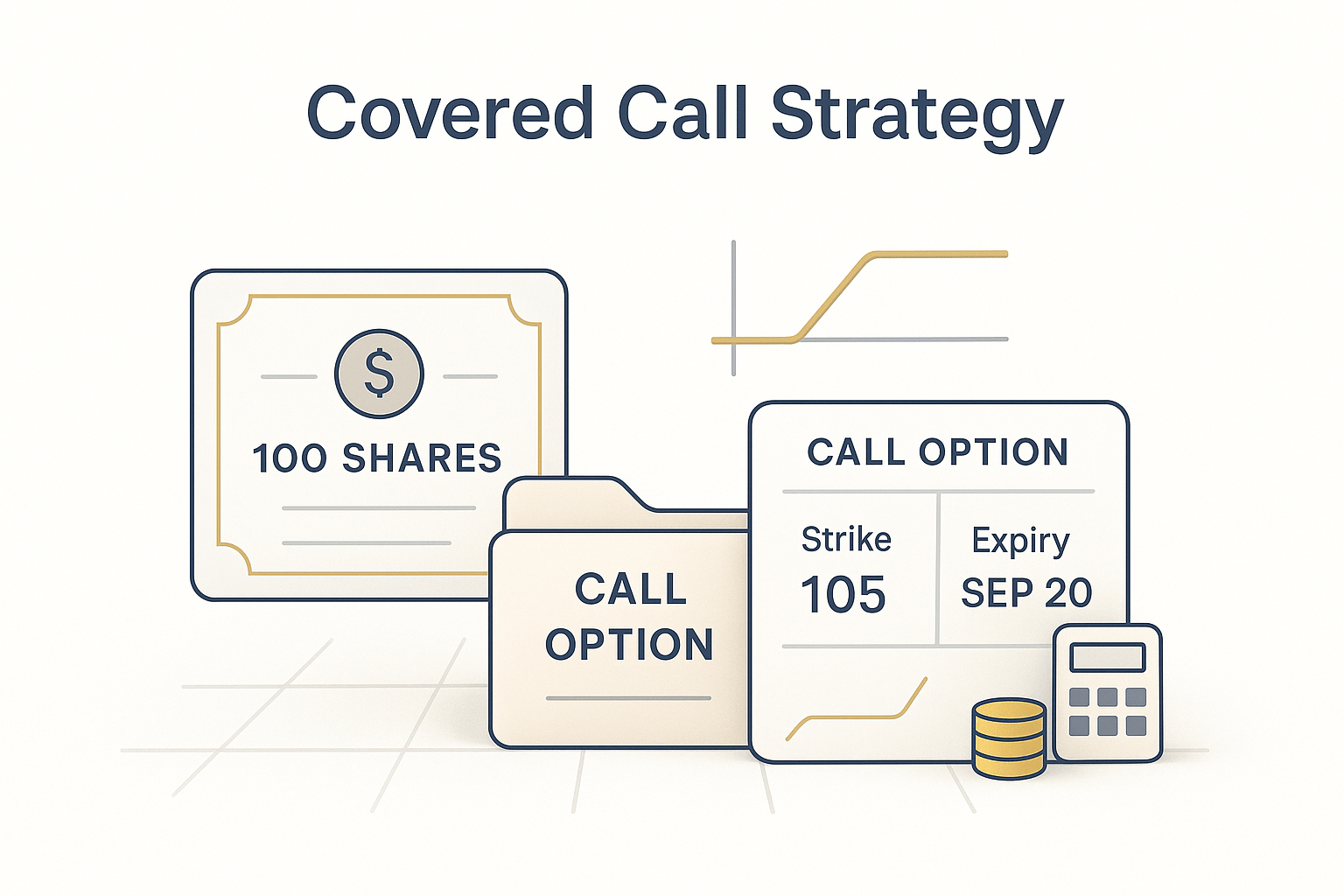

You own 100 shares of a stock (or ETF) and sell (write) one call option on the same ticker and expiry. The premium you receive adds income and a small cushion against declines. If price rises above the strike at expiration, your upside is capped and you may be assigned (shares sold at the strike).

- Goal: Earn option income on owned shares

- Best fit: Neutral to moderately bullish outlook

- Position size: 100 shares per call contract

How It Works (Step by Step)

- Own or buy 100 shares of the underlying per contract.

- Sell an out-of-the-money (OTM) call—often 1–8 weeks out.

- Collect premium → this lowers your cost basis.

- At expiry:

- If price ≤ strike: call expires worthless → keep shares + premium.

- If price > strike: likely assignment → shares sold at strike; keep premium.

Payoff at Expiration (Per Share)

| Underlying at Expiry | Position P/L | Comment |

|---|---|---|

| Below breakeven (Stock Price ≤ Entry − Premium) | Loss, reduced by premium | Premium cushions downside but does not remove it |

| Between breakeven and Strike | Profit grows with stock | Keep premium and shares |

| At or above Strike | Capped profit = (Strike − Entry) + Premium | Likely assigned; upside limited |

Numerical Example

You own 100 shares at ₹1,000. You sell a 1-month 1,060 call for ₹20. Outcomes at expiry:

| Spot at Expiry | Result | P/L per Share |

|---|---|---|

| ₹950 | Option expires; keep shares | −₹50 + ₹20 = −₹30 |

| ₹1,040 | Expires; keep shares | ₹40 + ₹20 = ₹60 |

| ₹1,080 | Assigned at ₹1,060 | (₹1,060 − ₹1,000) + ₹20 = ₹80 (max) |

Greeks You Actually Need

- Delta (≈ +0.25 to +0.35 OTM): Sets probability of assignment and premium size.

- Theta (> 0 to you): Time decay works in your favor; faster close to expiry.

- Vega (< 0): Premium shrinks if volatility falls; rises if volatility spikes.

- Gamma: Low for covered calls vs naked calls; risk mostly from the stock you own.

Why Use It

- Earn income while holding quality shares

- Small buffer against declines (premium)

- Behavioral benefit: rules reduce impulse trades

Key Trade-offs

- Upside is capped above the strike

- Stock risk remains on the downside

- Possible early assignment near ex-div dates

When a Covered Call Makes Sense

- You’re neutral to moderately bullish for the next 2–8 weeks.

- You’re happy to sell the stock at the strike (set target exits).

- Implied volatility is fair to rich vs its 6–12-month history.

- You prefer steady income over chasing full upside.

Construction Rules (Practical)

| Element | Guideline | Why |

|---|---|---|

| Strike selection | OTM call with delta ≈ 0.25–0.35 | Balanced income vs assignment risk |

| Expiry | 2–6 weeks | Good theta capture; manageable roll cadence |

| Roll plan | Buy back at ~75–85% of max profit or 7–10 days to expiry | Locks gains; reduces gap risk |

| Position size | Start small; match lots of 100 shares | Controls risk and slippage |

Operational Risks to Watch

- Assignment: Be prepared to deliver shares; set alerts near strike.

- Ex-dividend: Early exercise risk increases if call is ITM and dividend exceeds time value.

- Gap moves: Overnight news can jump price through the strike—have a roll/close rule.

- Liquidity: Prefer tight spreads and active options chains.

- Taxes: Premiums and stock sales may be taxed differently; consult a professional.

Covered Call Checklist (Apply Today)

Open checklist

Disclaimer

Education only—this is not investment, tax, or legal advice. Options involve risk and are not suitable for all investors.