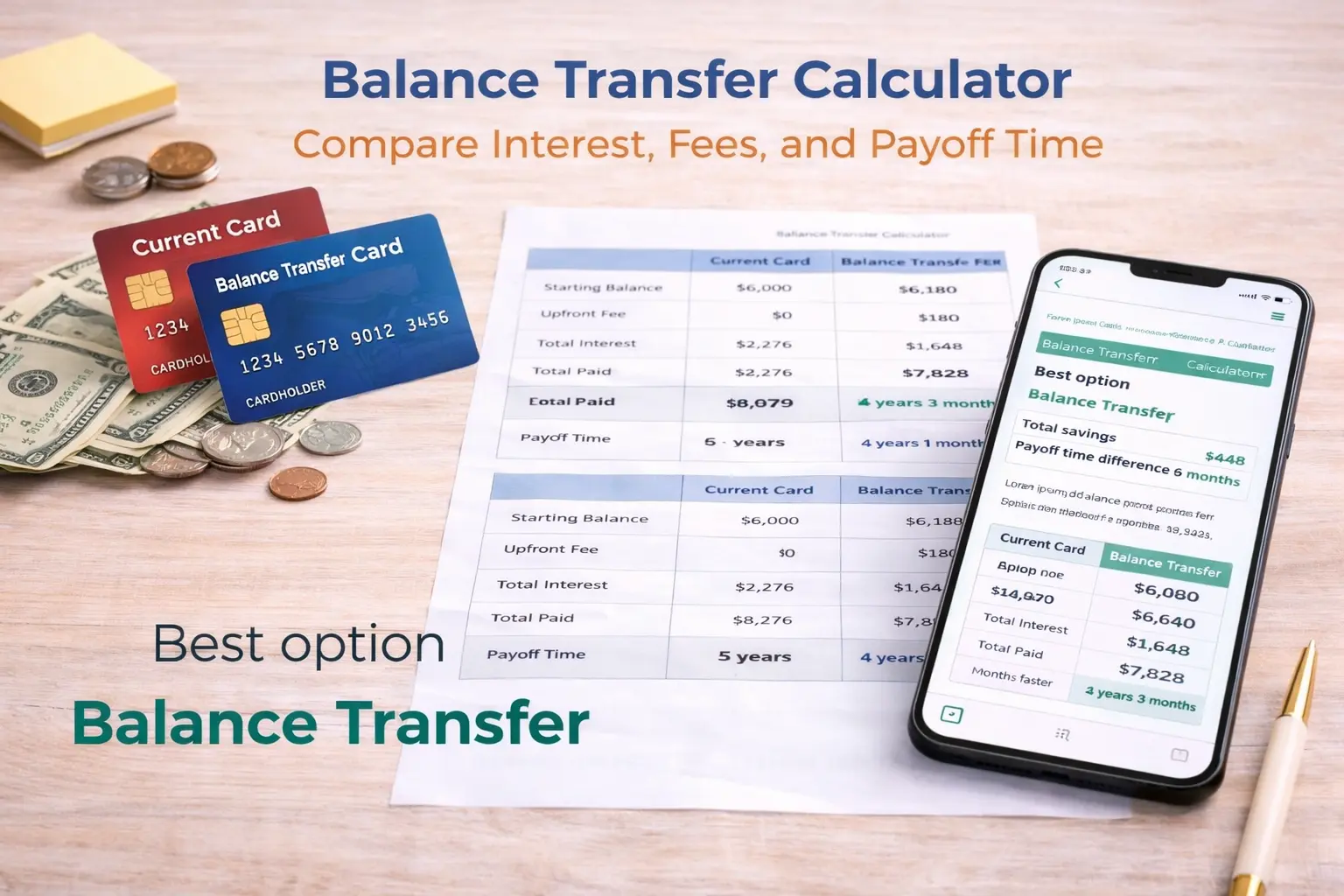

Balance Transfer Calculator: Compare Interest, Fees, and Payoff Time

A balance transfer can feel like an easy way to reduce interest, but the real benefit depends on the numbers. This page helps you compare two paths side by side so you can make a clear decision. You can estimate how much interest you may pay if you keep your balance on the current card. You can also estimate the cost of transferring to a new card that offers a 0 percent intro APR for a limited period. The calculator includes the balance transfer fee, which many people ignore while comparing offers. It also measures payoff time so you can see whether the move helps you become debt-free sooner. This is useful when you are trying to reduce monthly stress and improve cash flow. It is also useful when you want to decide whether a new card offer is truly better or just looks better.

Balance Transfer Calculator: Compare Interest, Fees, and Payoff Time

Use this calculator to compare keeping your current credit card balance versus transferring it to a new balance transfer card. It estimates upfront fees, interest charges, payoff time, and total cost based on your monthly payment.

Card To Transfer

This side models what happens if you keep the balance on your current card and keep paying the same monthly payment until it is paid off.

New Balance Transfer Card

Results

Best option

—

Total savings

—

Payoff time difference

—

Enter all values and click Calculate to compare costs. The model assumes a fixed monthly payment and monthly compounding.

How Balance Transfers Work in Real Life

A balance transfer moves an existing credit card balance to a new card, usually in exchange for promotional terms. The most common promotion is a 0 percent intro APR period that lasts for a set number of months. During this time, your payment reduces the principal faster because interest is not added each month. However, most cards charge a transfer fee, often a percentage of the balance you move. That fee can reduce or even remove the benefit if your balance is small or if you pay it off slowly. After the intro period ends, the card switches to a regular APR, which may be high. If you still have a balance at that point, interest resumes and can grow quickly. Because of these details, a balance transfer works best when you have a strong payoff plan and stable monthly payments.

What You Need to Enter Before You Calculate

To get meaningful results, you should enter values that match your current situation rather than rough guesses. Start with the current balance you want to pay down, using the amount shown on your latest statement. Next, enter your current card APR, which is often listed as a purchase APR on your card account page. Then choose a monthly payment amount that you can realistically maintain without missing payments. On the new card side, enter the balance transfer fee percentage offered by the card. Add the length of the 0 percent intro APR period in months, because this affects how much principal you can remove without interest. Finally, enter the regular APR that applies after the intro period ends, since this will determine the cost if you carry a balance beyond the promotion. When you enter clean data, the calculator can provide a comparison that feels realistic and actionable.

Understanding the Transfer Fee and Why It Matters

The balance transfer fee is an upfront cost that is usually added to your new card balance immediately. For example, if you transfer a balance and pay a percentage fee, you start the new card with more debt than you moved. That means your monthly payments must cover both the original balance and the fee. If your fee is high and the intro period is short, the fee can outweigh the interest savings. This is why the calculator includes the fee in the balance transfer path rather than ignoring it. It also helps you see how quickly you need to repay the balance for the transfer to make sense. In many cases, the best balance transfer is the one you can pay off during the intro period. When you treat the fee as a real cost, your decision becomes more accurate and less emotional.

How Payoff Time Changes Your Total Cost

Payoff time is not just a convenience number, it changes how much interest builds up. If you pay the balance off faster, you reduce the time interest has to accumulate. If you pay slowly, the balance stays higher for longer and interest becomes a larger part of your total cost. A 0 percent intro period can shorten payoff time because it puts your payment directly against principal. However, if the intro period ends while you still have a large balance, the regular APR can bring the cost back up quickly. The calculator shows payoff time for both the current card and the new transfer card using the same monthly payment. This makes it easier to understand whether the transfer helps you exit debt sooner. It also helps you decide if you should increase your monthly payment during the intro period to maximize the benefit.

How to Read the Results and Choose the Better Option

After you click calculate, you will see a clear comparison of total interest, total paid, and payoff time. The best option is the one with the lower total paid, because that reflects the true cost of your debt payoff plan. If totals are close, payoff time becomes an important secondary factor because being debt-free earlier reduces risk. You should also look at the savings figure, which shows the difference between the two paths. If the balance transfer produces meaningful savings and a shorter payoff time, it usually indicates a strong match for your situation. If savings are small or negative, it often means the fee or the post-intro APR removes the advantage. The result is not just a number, it is a decision guide that tells you what conditions make a transfer worthwhile. If the calculator shows that neither option pays off, it means your monthly payment is too low compared to the interest cost, and you may need a larger payment strategy.

Practical Tips to Get the Most from a Balance Transfer

A balance transfer works best when you treat the intro period like a deadline rather than a comfort zone. You can aim to pay the balance down as much as possible before the regular APR starts. You can also avoid using the new card for purchases because some cards apply different APR rules to new spending. You should consider setting up autopay so you do not miss a due date and risk losing promotional terms. If you can increase your payment slightly during the intro months, you often create more savings than expected. You should also check whether the new card has a minimum fee or a maximum cap, because that changes the economics. A careful plan makes the transfer a tool for payoff rather than a way to postpone the problem. When you combine discipline with clear numbers, balance transfers can reduce interest and improve your financial momentum.

Important Notes and Limitations

This calculator is designed to estimate outcomes using standard monthly compounding and a fixed payment assumption. Real credit cards may calculate interest slightly differently depending on daily balances and statement cycles. The tool also assumes you do not add new purchases or cash advances while paying down the balance. If you continue to spend on the card, payoff time and cost can change significantly. The calculator includes the transfer fee as part of the new balance because that reflects how many issuers apply it. It also assumes the regular APR begins immediately after the intro period ends if any balance remains. Results are meant for planning and comparison, not as financial advice. You should always verify the exact terms of your card offer before you apply or transfer a balance. Use this page as a clear decision framework and then confirm your final details with the issuer.